The Federal Finance Act, 2025 introduces important amendments to the Income Tax Ordinance, 2001 that directly impact individual taxpayers. In simple terms, here’s a breakdown of the revised tax rates and key regulatory changes affecting salaried individuals, associations of persons (AOP) and business proprietors.

Revised Slab Rates for Salaried Individuals

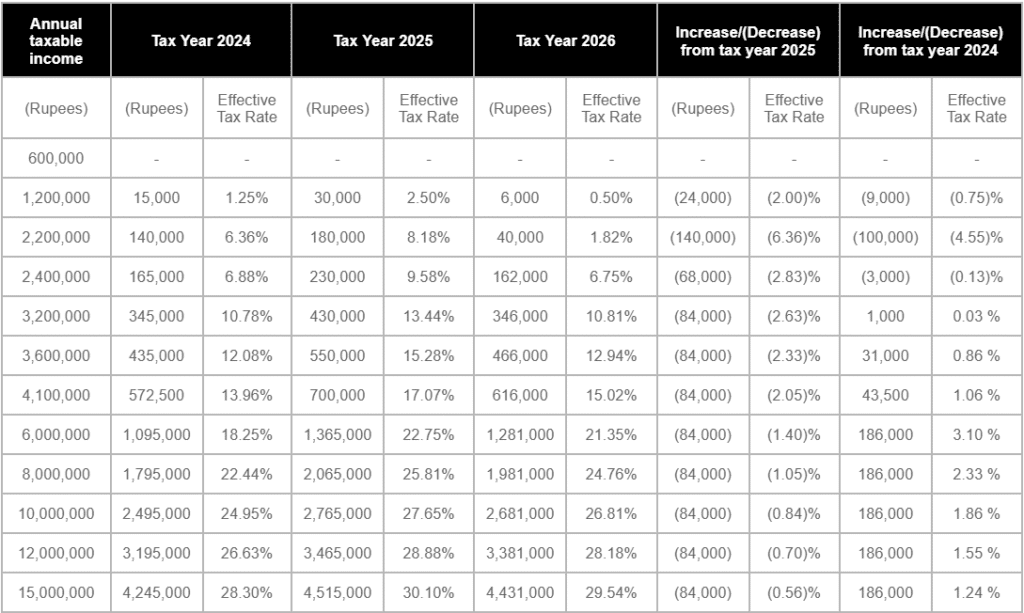

The slab rates for salaried individuals have been revised through the Finance Act 2025. The maximum rate remains 35%, but incremental rates have been adjusted across slabs, and the surcharge for salaried individuals earning above Rs. 10 million has been reduced from 10% to 9%.

This provides relief in some brackets while maintaining progressivity in the income tax rates for salaried persons in Pakistan.

For salary tax calculations and practical tax-saving tips, use our online salary tax calculator for Pakistan. Below is a clear and easy-to-read comparison of the revised income tax slab rates for salaried individuals under the Finance Act 2025 for quick reference

| Sr No. | Taxable income | Previous Rates | New Rates |

|---|---|---|---|

|

1 |

Upto Rs 600,000 |

0%

|

–

|

|

2.

|

Exceeding Rs 600,000 upto Rs 1,200,000

|

5% of the amount exceeding Rs 600,000

|

1% of the amount exceeding Rs 600,000 |

|

3.

|

Exceeding Rs 1,200,000 upto Rs 200,000

|

15% of the amount

exceeding Rs 1,200,000

|

11% of the amount

exceeding Rs 1,200,000

|

|

4.

|

Exceeding Rs 2,200,000 upto Rs 200,000

|

25% of the amount

exceeding Rs 2,200,000

|

23% of the amount

exceeding Rs 2,200,000

|

|

5.

|

Exceeding Rs 3,200,000 upto Rs 100,000

|

30% of the amount

exceeding Rs 3,200,000

|

30% of the amount

exceeding Rs 3,200,000

|

|

6.

|

Exceeding Rs 4,100,000

|

35% of the amount

exceeding Rs 4,100,000

|

35% of the amount

exceeding Rs 4,100,000

|

The impact of the above-mentioned changes in slabs (other than surcharge and super tax) is illustrated as under:

Tax on Pension Income Exceeding Rs 10 Million in Pakistan

The Finance Act 2025 has significantly revised the tax treatment of pension income in Pakistan, particularly for high-value pensions. Under the newly inserted provisions of sections 12(2A) and 149(1A) of the Income Tax Ordinance, 2001 [Ordinance], read with Clauses 8 and 9 of Part I of the Second Schedule, a final tax is now applicable on pensions received from a former employer in excess of Rs 10 million in a tax year by an individual under the age of 70 years.

The impact of the above-mentioned changes in slabs (other than surcharge and super tax) is illustrated as under:

Revised Tax Rates on Pension Income

| Sr No. | Description | Rate of Tax |

|---|---|---|

|

1.

|

Where the amount of pension received does not exceed Rs. 10 million

|

0%

|

|

2.

|

Where the amount of pension received exceeds

Rs 10 million

|

5% of the amount exceeding Rs 10 million

|

This amendment marks a major shift in the taxation of pension benefits in Pakistan, directly impacting retirees with substantial pension payouts.

Exceptions and Special Cases

If an individual continues to work for the former employer or its associated companies, this final tax on pension income will not apply. Instead, the pension will be taxed according to the individual’s normal income tax slab applicable to salaried or non-salaried persons.

Furthermore, the Finance Act 2025 has withdrawn the longstanding tax exemption on pension income received by members of the Armed Forces of Pakistan or Federal/Provincial Government employees. Nevertheless, pension benefits granted to families or dependents of public servants or armed forces personnel who die during service remain exempt under the relevant pension rules.

Withholding Tax Obligations

Under section 149(1A) of the Ordinance, any person responsible for paying pension to an individual below 70 years of age is now required to withhold income tax on pension amounts exceeding Rs. 10 million at the prescribed 5% rate, along with the surcharge under Section 4AB. Such withholding must be applied after allowing admissible tax credits and adjustments.

Interestingly, while section 12 of the Ordinance refers to final tax on pension income, no corresponding amendments have yet been made to sections 8 and 169 governing the final tax regime under the Ordinance. The FBR (Federal Board of Revenue) is expected to issue a clarification on this point to address potential compliance concerns.

Restrictions on Economic Transactions

The Finance Act 2025 has formally introduced the concept of “Eligible Persons” under Section 114C of the Income Tax Ordinance, 2001 read with the newly inserted Fifteenth Schedule, placing strict restrictions on economic transactions in Pakistan for ineligible persons. This measure aims to curb undocumented investments and ensure compliance with the FBR’s tax return filing requirements.

Initially proposed under the Tax Laws (Amendment) Bill 2024, this regime was passed with modifications through the Finance Act 2025, making it a major step toward regulating high-value transactions across the economy.

Key Restrictions for Ineligible Persons

Below is an overview of the major economic transaction restrictions for ineligible persons as prescribed under the 15th Schedule of the Income Tax Ordinance:

| Transaction Restriction | Value Specification | Threshold Limitation for Ineligibility |

|---|---|---|

|

Motor Vehicle Purchase / Registration Applications for booking, purchasing, or registering locally manufactured or imported motor vehicles exceeding the threshold will not be accepted by manufacturers or the Excise & Taxation Registration Authority if made by ineligible persons.

|

Invoice value for locally manufactured vehicles or import value as assessed by Customs (inclusive of all taxes, duties, levies and charges).

|

Exceeding Rs. 7 million per motor vehicle.

|

|

Immovable Property Transactions Applications or requests by ineligible persons to authorities for registering, recording, or attesting transfers of immovable property beyond the threshold will be restricted.

|

Fair Market Value as defined in Section 2(22AA) of the Ordinance.

|

Exceeding Rs. 100 million per immovable property.

|

|

Securities / Mutual Funds / Investment Accounts Authorized persons are prohibited from opening or maintaining accounts in respect of securities, units of mutual funds or similar investments if the total investment by an ineligible person exceeds the threshold (new investments only; excludes reinvestments of similar securities or reinvestment of returns).

|

Acquisition cost of securities, debt securities, units of mutual funds or money market instruments.

|

Exceeding Rs. 50 million.

|

|

Cash Withdrawals Banking companies are restricted from allowing cash withdrawals from any bank account of a person in excess of the annual threshold.

|

–

|

Rs. 100 million across all bank accounts held by an individual.

|

Compliance Requirements for Eligible Persons

Any person undertaking transactions above the specified thresholds must demonstrate “sufficient resources” through either their last filed income tax return and wealth statement or by submitting a Sources of Investment and Expenditure Statement on the FBR portal. Under the rules, sufficient resources are defined as 130% of cash and cash equivalent amounts declared, including fair market value of gold, net realizable value of stocks, bonds, receivables or any other prescribed cash equivalents.

However, filing such a statement or demonstrating sufficient resources does not provide immunity under Section 111 regarding unexplained income or assets. The Federal Board of Revenue (FBR) retains the power to initiate proceedings for any unsubstantiated funds.

Exemptions from Restrictions

- Non-resident persons and public companies are exempt from these restrictions except for the cash withdrawal limit from bank accounts.

- The Federal Government may notify the effective date for enforcement of these restrictions and may adjust the thresholds (reduce or enhance) through official Gazette notifications.

Definitions for Section 114C – Finance Act 2025

- Eligible Person: An individual or entity (including immediate family members) who has filed an income tax return for the preceding tax year and has sufficient resources in their wealth statement (for individuals) or financial statements (for companies/AOPs), or has declared resources through a Sources of Investment and Expenditure Statement.

- Ineligible Person: A person who does not meet the above criteria.

- Immediate Family Member: Includes an individual’s parents, spouse and dependent children.

- Sources of Investment and Expenditure Statement: A declaration filed electronically on the FBR’s web portal specifying the sources of funds used for transactions.

- Sufficient Resources: At least 130% of declared cash or cash equivalents, including fair market value of gold, net realizable value of stocks, bonds, receivables or other prescribed assets, as disclosed in the wealth statement or financial statements attached to the income tax return.

Where an asset is purchased by way of exchange of capital assets already declared, the disposal of such capital assets will be treated as part of cash equivalents to the extent of the value mentioned in the agreement.

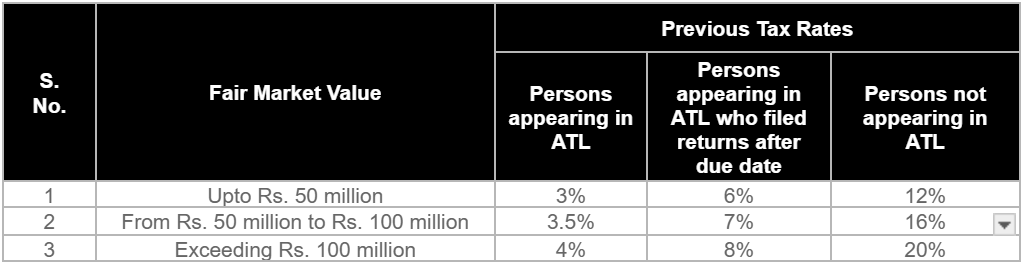

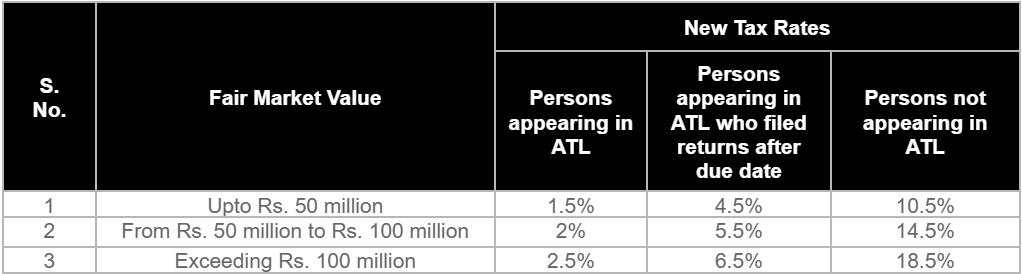

Advance Tax on Purchase, Sale, and Transfer of Immovable Property

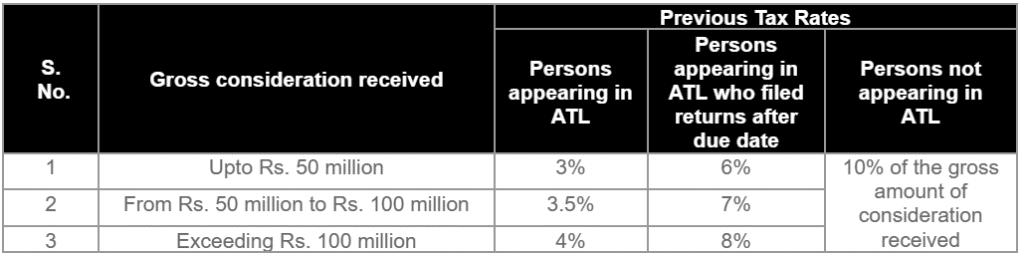

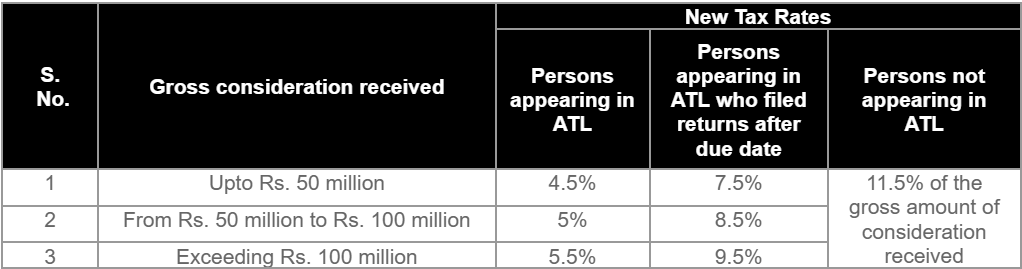

The advance tax on immovable property transactions has been revised upward for sellers and downward for purchasers. Persons appearing on the Active Taxpayers List (ATL) face different rates compared to late filers and non-filers.

Advance Tax on Sale or Transfer of Immovable Property

Advance Tax on Purchase of Immovable Property

This adjustment affects the property market in Pakistan and aims to enhance compliance with real estate tax rules under the Tenth Schedule.

Exchange of Banking and Tax Information Related to High Risk Persons

The Finance Act 2025 has introduced new provisions under section 175AA of Ordinance, enabling the Federal Board of Revenue (FBR) to obtain banking information on high-risk persons directly from Scheduled Banks in Pakistan. This measure strengthens tax compliance and enhances the detection of undisclosed income and assets.

Key Provisions under Section 175AA

Based on information provided by the FBR to commercial banks, including turnover, taxable income, bank account numbers declared in income tax returns, identification data, and other information compiled using data-based algorithms, the Scheduled Banks will now be required to share back the following particulars:

- Name of the account holder;

- Account numbers of such persons;

- Any other banking details where the bank’s records vary from the FBR’s data algorithms.

This exchange of banking and tax information will allow the FBR to match income declared in tax returns with actual banking transactions of high-risk individuals or classes of persons.

Overriding Effect & Confidentiality

These provisions have an overriding effect over all other laws, including the Banking Companies Ordinance, 1962, ensuring that Scheduled Banks’ reporting obligations to the FBR take priority. However, the banking information received by the FBR under Section 175AA shall be used strictly for tax purposes and will remain confidential under the Income Tax Ordinance, 2001.

Why Section 175AA Matters

By linking bank account data with tax records through FBR’s advanced data algorithms, this provision aims to:

- Detect undisclosed income and assets;

- Reduce tax evasion by high-risk persons;

- Strengthen Pakistan’s anti-money laundering and tax transparency efforts;

- Increase bank-FBR coordination for better tax enforcement.

Advance Tax on Cash Withdrawals by Non-Filers

The rate of advance tax on cash withdrawals exceeding Rs. 50,000 per day by non-filers (persons not appearing on the Active Taxpayers List) has been increased from 0.6% to 0.8%. This move discourages large cash transactions by non-filers and encourages filing of income tax returns in Pakistan.

Restoration of Tax Rebate to Full-Time Teachers and Researchers

Earlier, an exclusion was provided for the increase in withholding tax rate on capital gains under section 37A of the Ordinance. This exclusion is now restricted for securities acquired on or after July 1, 2025, increasing tax compliance on capital market transactions in Pakistan.

Tax Withholding on Gain on Disposal of Securities

Before the Finance Act 2025, a business could set off its losses under one head of income (other than capital loss) against income under any other head of income, excluding salary. The Finance Act 2021 had relaxed this by allowing business losses to be adjusted against property income.

The Finance Act 2025 has now reinstated the pre-2021 restriction, once again barring the adjustment of business loss against property income. This reversal narrows loss utilisation and requires businesses to reassess their tax planning strategies.

Posting of Officer of Inland Revenue

The Finance Act 2025 has inserted section 175C in the Ordinance, empowering the Federal Board of Revenue (FBR) and the Chief Commissioner Inland Revenue to post Inland Revenue officers at business premises of any person or class of persons.

This provision allows real-time monitoring of business activities, production, supply of goods or services, and stock of unsold goods to ensure correct reporting and tax compliance in Pakistan. While the measure aims to curb tax evasion and improve transparency, businesses may be concerned about possible interference. Appropriate rules and procedures are required to ensure fair implementation of this power.

Disclosure of Tax Information by Public Servants

Section 216 of the Ordinance safeguards taxpayer confidentiality by restricting unauthorized disclosure of tax-related information by public servants. Through the Finance Act 2025, this section has been amended to include new categories of permissible recipients of confidential taxpayer data under strict conditions:

- Auditors appointed on a contractual basis or via third parties (including payroll firms) assisting taxation officers under Section 207, subject to non-disclosure agreements.

- The Tax Policy Office for processing and analyzing data for research and policy analysis.

- Recognized universities and international donor agencies, provided the taxpayer’s data is anonymized before sharing.

This amendment balances data sharing for policy purposes with taxpayer privacy.

Final Thoughts on the Federal Finance Act 2025

With revised income tax slab rates, a new final tax on high-value pension income, stricter economic transaction restrictions for ineligible persons, and enhanced FBR–bank data sharing under section 175AA of the Ordinance, the Act strengthens tax compliance, limits undocumented investments, and promotes financial transparency.

At the same time, measures like the reduced surcharge on high-income earners, reinstatement of the 25% tax rebate for full-time teachers and researchers until tax year 2025, and adjustments in advance tax on immovable property transactions reflect a more balanced approach to revenue generation and taxpayer relief.

Collectively, these reforms modernize Pakistan’s taxation system, align high-value transactions with declared resources, and create a more transparent, equitable, and growth-oriented fiscal environment for individuals, businesses, and investors.

FAQs - Relating to Salaried and Non-Salaried Persons

Q1. What is the Federal Finance Act 2025 and how does it affect individual taxpayers in Pakistan?

The Federal Finance Act 2025 introduces wide-ranging amendments to the Income Tax Ordinance, 2001. It revises income tax slab rates for salaried individuals, imposes a final tax on high-value pensions, restricts certain economic transactions for “ineligible persons,” and strengthens data sharing between banks and the Federal Board of Revenue (FBR) to improve tax compliance and transparency.

Q2. What are the revised income tax slab rates for salaried individuals under the Finance Act 2025?

While the maximum rate remains 35%, incremental rates have been lowered in several brackets. For example, income between Rs. 600,000 and Rs. 1,200,000 is now taxed at 1% (down from 5%) and income between Rs. 1,200,000 and Rs. 2,200,000 at 11% (down from 15%). The surcharge on salaried persons earning above Rs. 10 million has been reduced from 10% to 9%.

Q3. How does the Finance Act 2025 tax pension income exceed Rs. 10 million?

A final tax at 5% now applies to pension income received from a former employer exceeding

Rs. 10 million per tax year for individuals under 70 years of age. Pension below Rs. 10 million remains tax-free. If the retiree is still working with the former employer or an associated company, normal income tax slab rates apply instead.

Q4. Are Armed Forces and government pensions still exempt from income tax?

No. The Finance Act 2025 has withdrawn the longstanding tax exemption on pension income for Armed Forces members and Federal/Provincial Government employees. However, pensions granted to families or dependents of public servants or armed forces personnel who die during service remain exempt under the relevant pension rules.

Q5. What are “eligible” and “ineligible” persons under Section 114C of the Ordinance?

An “eligible person” is an individual or entity that files an income tax return and shows sufficient resources (at least 130% of declared cash and cash equivalents) in their wealth statement or financial statements. An “ineligible person” does not meet these criteria.

Q6. What transactions are restricted for ineligible persons in Pakistan?

Ineligible persons cannot book, purchase or register locally manufactured or imported motor vehicles exceeding Rs. 7 million, transfer immovable property exceeding Rs. 100 million, invest in securities/mutual funds above Rs. 50 million (new investments only), or withdraw cash exceeding Rs. 100 million annually from bank accounts.

Q7. How has advance tax on purchase, sale and transfer of immovable property changed?

The Finance Act 2025 increases advance tax rates for sellers and decreases rates for purchasers, with different rates for Active Taxpayers List (ATL) filers, late filers and non-filers. For instance, non-filers now face up to 11.5% advance tax on sales of property up to Rs. 50 million and up to 18.5% on purchases exceeding Rs. 100 million.

Q8. What is Section 175AA and why is it important?

Section 175AA allows the FBR to directly obtain banking information of high-risk persons from Scheduled Banks in Pakistan. This enables the FBR to match bank transactions with declared income, detect undisclosed income or assets, reduce tax evasion, and strengthen anti-money laundering efforts while maintaining confidentiality under the Income Tax Ordinance, 2001.

Q9. What is the new advance tax rate on cash withdrawals by non-filers?

The rate of advance tax on cash withdrawals exceeding Rs. 50,000 per day by non-filers has been increased from 0.6% to 0.8%, encouraging more individuals to file income tax returns.

Q10. Has the tax rebate for full-time teachers and researchers been restored?

Yes. The 25% tax rebate for full-time teachers and researchers, withdrawn by the Finance Act 2022, has been reinstated retroactively from 1 July 2022 and will remain effective until the end of tax year 2025.

Q11. What does Section 175C (posting of officers) mean for businesses?

Section 175C empowers the FBR or the Chief Commissioner Inland Revenue to post officers at business premises for real-time monitoring of production, supply of goods or services, and stock levels. This measure is designed to improve compliance but will require clear rules to avoid undue interference.

Q12. How does Section 216 now handle disclosure of taxpayer information?

Section 216 continues to protect taxpayer confidentiality but has been amended to allow controlled sharing of anonymized data with auditors, the Tax Policy Office, recognized universities and international donor agencies for research and policy purposes under strict non-disclosure agreements.

What do you think?

bgbc3j

vnmid2

k0f6w3

照片令人惊艳。由衷感谢 感受。

sms activate login sms activate login .

мостбет кэшбэк условия https://mostbet61527.help/

sms activation github.com/SMS-Activate-Alternatives .

как скачать mostbet на iphone https://mostbet61527.help

mostbet номер телефона поддержки mostbet номер телефона поддержки